What is a Lien?

A lien is a legal claim or right against a property that allows the lien holder to keep possession of the property until a debt is paid. Liens are commonly used to secure repayment of a debt or obligation. When a lien is placed on a property, it essentially gives the lien holder an ownership interest in the property until the debt is satisfied.

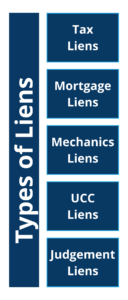

There are several different types of liens that can be attached to a property, including:

Tax Liens: These are liens placed by government entities for unpaid property taxes, income taxes, or other tax debts. Tax liens take priority over most other liens.

Mortgage Liens: When you take out a mortgage to purchase a home, the lender places a lien on the property to secure the loan. This gives the lender a claim against the home if you default on the mortgage payments.

Mechanic’s Liens: Contractors, subcontractors, or suppliers who perform work or provide materials for home improvements can place a mechanic’s lien on the property if they are not paid for their services.

Judgment Liens: If a court rules that you owe a debt, the creditor can obtain a judgment lien against your property to secure repayment of the judgment.

Liens are attached to the property itself, not just the current owner. This means that when you sell a home, any outstanding liens must be paid off from the sale proceeds before you can receive your share of the money. Failure to pay off existing liens could result in the lien holder initiating foreclosure proceedings or placing a levy on the sale. We are experts in property liens in the Richmond market and stand ready to assist you – as a premier “We Buy Houses in Richmond, VA” company.

Make sure you fully do your research before faced with property liens by reading the following posts: How to Handle Property Liens When Selling a House in Richmond, VA, plus Contact the Lien Holder, Consider Selling to a Cash Home Buyer, Work with a Real Estate Agent, and Tips for Selling a Home With Liens.

Why It’s Crucial to Identify and Resolve Liens

Identifying and resolving any outstanding liens on your property is a critical step when selling a house. Liens are legal claims or encumbrances against your property, often resulting from unpaid debts or obligations. Failing to address these liens can have severe consequences and potentially derail the entire sale process.

When a lien is placed on your property, it grants the lien holder a legal interest in your home. This means that if you attempt to sell the property without resolving the lien, the lien holder has the right to collect the outstanding debt from the sale proceeds. In some cases, the lien holder may even have the authority to prevent the sale from going through until the lien is satisfied.

Unresolved liens can create significant roadblocks during the sale process. Potential buyers and their lenders will typically conduct a title search to ensure that the property has a clear and marketable title. If any liens are discovered, it can raise red flags and make buyers hesitant to proceed with the purchase. Lenders may also refuse to provide financing if there are outstanding liens on the property, as their interest would be subordinate to the existing lien holders.

Furthermore, if you fail to disclose known liens to potential buyers, you could be held liable for misrepresentation or fraud. This could result in legal disputes, costly lawsuits, and potential financial penalties.

Addressing and resolving liens is crucial to ensure a smooth and successful sale. By taking proactive steps to identify and satisfy any outstanding liens, you can provide a clear title to the new buyer, avoid potential legal complications, and increase the chances of a successful and hassle-free transaction.

Primary Lien from Mortgage Lender

When selling a house, the primary lien that most homeowners need to address is the mortgage lien held by their lender. This lien secures the loan that was used to purchase the property. Until the mortgage is fully paid off, the lender maintains a legal claim on the home as collateral for the outstanding loan balance.

To sell the house, the existing mortgage must be paid in full through a process called mortgage payoff. The payoff amount includes the remaining principal balance, accrued interest, and any other fees or charges outlined in the loan agreement. The buyer’s funds or new mortgage will go towards satisfying this payoff amount owed to the original lender.

Once the payoff is completed, the lender will issue a lien release or mortgage satisfaction document. This legally certifies that the debt has been settled, and the lien on the property is removed. The lien release is a crucial step, as it clears the way for the home’s title to transfer cleanly to the new owner without any outstanding claims or debts attached.

Homeowners should work closely with their lender, escrow company, and real estate professionals to ensure the mortgage payoff and lien release process goes smoothly during the sale. Any delays or errors could potentially derail or postpone the closing until the lien is officially removed from the property’s title records.

Unpaid Property Taxes and Tax Liens

When selling a house, it’s crucial to address any outstanding property tax debts to avoid tax liens. A tax lien is a legal claim placed on a property by a government entity (state, county, or municipality) for unpaid property taxes. This lien gives the taxing authority the right to seize the property and sell it to recover the delinquent taxes, interest, and penalties.

To determine if your property has a tax lien, you’ll need to research the tax records with the appropriate government office, typically the county tax assessor or treasurer’s office. These records will show if there are any delinquent taxes owed and if a lien has been placed on the property.

If a tax lien exists, you’ll need to satisfy the lien requirements before selling the house. This typically involves paying off the full amount owed, including the delinquent taxes, interest, and any applicable penalties or fees. Once the lien is satisfied, the government entity will issue a lien release, which removes the legal claim on the property.

Failing to address a tax lien can significantly complicate the home sale process and may prevent the transfer of a clear title to the new buyer. It’s essential to research the property’s tax status early and take the necessary steps to resolve any outstanding tax liens before listing the house for sale.

Understanding Contractor Liens

Contractor liens, also known as mechanic’s liens, are legal claims that contractors, subcontractors, or suppliers can file against a property when they have not been fully paid for their work or materials. These liens can pose a significant challenge when selling a house, as they create a cloud on the property’s title and can prevent the transfer of ownership until the debt is resolved.

When homeowners hire contractors for home improvement projects, they typically sign a contract that outlines the scope of work, payment terms, and other conditions. If the homeowner fails to pay the contractor as agreed, the contractor has the right to file a lien against the property, which serves as a legal claim against the property’s value.

It’s crucial to obtain lien waivers from all contractors, subcontractors, and suppliers involved in any home improvement project. A lien waiver is a legal document that confirms the contractor has been paid in full and waives their right to file a lien against the property. Without proper lien waivers, even if the homeowner has paid the general contractor, subcontractors or suppliers may still be able to file liens if they were not paid by the general contractor.

If a contractor lien is discovered during the home selling process, it’s essential to address it promptly. The homeowner can either pay the outstanding debt to remove the lien or negotiate a settlement with the contractor. In some cases, the homeowner may need to seek legal assistance to resolve the issue, especially if the lien is disputed or the contractor is uncooperative.

Failing to resolve open contractor liens can significantly delay or even derail the home sale process, as most lenders and title companies will not allow the transfer of ownership until the liens are cleared. This can result in lost time, additional legal fees, and potential deal-breaker for prospective buyers.

Judgment Liens

Judgment liens can arise when a creditor obtains a court judgment against you for an unpaid debt, such as credit card debt, personal loans, or other financial obligations. These liens can attach to your real estate property, including your home.

When a creditor secures a judgment against you, they may record a lien against your property with the county recorder’s office. This lien gives the creditor a legal claim against your property, which can complicate the sale process.

To sell your home with a judgment lien, you typically have a few options:

- Pay off the lien: You can satisfy the judgment by paying the outstanding debt in full, including any accrued interest and fees. Once paid, the creditor should provide a lien release, which you can record to remove the lien from your property.

- Negotiate a settlement: You may be able to negotiate a reduced payoff amount with the creditor in exchange for a lien release. This option can be more affordable than paying the full amount owed.

- Use sale proceeds to pay off the lien: If the sale proceeds from your home are sufficient, you can pay off the judgment lien at closing. The lien amount will be deducted from your proceeds, and the lien will be released.

- Short sale or foreclosure: In some cases, if the outstanding debt exceeds the value of your home, you may need to consider a short sale (with the lender’s approval) or allow the property to go into foreclosure.

It’s crucial to address any judgment liens before selling your home, as they can create complications and delays in the sale process. Consulting with a real estate attorney or a reputable title company can help you understand your options and ensure a smooth transaction.

Searching Property Records

When selling a house, it’s crucial to conduct a comprehensive search of property records to identify any potential liens or encumbrances on the property. There are several options available for searching property records, each with its own advantages and limitations.

One option is to perform a title search, which involves hiring a professional title company or attorney to examine the property’s chain of title and uncover any outstanding liens or other issues. A title search is generally considered the most thorough method, as it involves a detailed review of public records, court documents, and other relevant sources.

Alternatively, many counties and municipalities now offer online access to property records, allowing homeowners to search for liens and other information themselves. While these online databases can be a convenient and cost-effective option, it’s important to note that they may not always be complete or up-to-date, and there is a risk of missing important information.

Regardless of the method chosen, it’s essential to conduct a thorough search of property records to ensure that any existing liens are identified and addressed before attempting to sell the property. Failing to do so could result in delays, legal complications, or even the inability to transfer ownership to the new buyer.

Resolving Different Types of Liens

When selling a house, it’s crucial to address any existing liens to ensure a smooth transaction. Here are the steps to resolve different types of liens:

Mortgage Liens

Mortgage liens are typically the most common and straightforward to resolve. Contact your lender and request a payoff quote, which includes the remaining balance, interest, and any applicable fees. Once you have the payoff amount, you can arrange for the lender to be paid from the sale proceeds at closing.

Tax Liens

Tax liens are imposed by government entities for unpaid property taxes. To resolve a tax lien, you’ll need to pay the outstanding taxes, interest, and penalties in full. Contact the relevant tax authority to obtain the payoff amount and make arrangements for payment from the sale proceeds.

Mechanic’s Liens

Mechanic’s liens are filed by contractors or suppliers who have not been paid for work or materials provided for home improvements or repairs. Resolving these liens may involve negotiating a settlement or paying the outstanding amount in full. Obtain a lien release from the contractor or supplier once the debt is satisfied.

Judgment Liens

Judgment liens are court-ordered liens resulting from unpaid debts, such as credit card balances or personal loans. To remove a judgment lien, you’ll need to negotiate a settlement with the creditor or pay the outstanding amount in full. Obtain a lien release from the creditor once the debt is satisfied.

Disputing Invalid Liens

In some cases, liens may be filed erroneously or without proper justification. If you believe a lien is invalid, you can dispute it by providing evidence and documentation to the appropriate authority. This may involve filing a formal objection or seeking legal assistance.

Regardless of the lien type, it’s essential to obtain lien releases from the respective parties once the debts are satisfied. These releases serve as proof that the liens have been cleared, allowing for a smooth transfer of ownership during the sale process.

Situations Where Sale May Proceed with Liens (Lien Assumed by Buyer)

When selling a house with an existing lien, one option is for the buyer to assume responsibility for the lien. This means the buyer agrees to take over the remaining payments or obligations associated with the lien. In such cases, the sale can proceed, but there are pros and cons to consider, as well as additional requirements.

Pros:

- Allows the sale to go through without the seller having to pay off the entire lien upfront.

- The buyer may be able to negotiate a lower purchase price by taking on the lien.

- Certain types of liens, such as mortgage loans, may have favorable interest rates that the buyer can benefit from by assuming them.

Cons:

- The buyer becomes responsible for the lien, which can impact their finances and credit.

- The lien may have unfavorable terms or high remaining balances that the buyer must take on.

- The lien holder (e.g., lender or creditor) must approve the assumption, which may involve additional fees or requirements.

Additional Requirements:

- The lien holder must agree to the assumption and may require the buyer to meet specific credit and income qualifications.

- A new agreement or contract may need to be drafted and signed by the buyer, assuming the lien’s terms and conditions.

- The buyer should thoroughly review the lien’s details, including the remaining balance, interest rate, and repayment terms, before agreeing to assume it.

- The seller may need to provide documentation and disclosures related to the lien to the buyer during the sale process.

It’s essential for both the buyer and the seller to carefully evaluate the pros and cons of assuming a lien and to consult with legal and financial professionals to ensure a smooth and compliant transaction.

Assistance from Title Companies and Attorneys

When selling a house, it’s crucial to determine and address any existing liens to ensure a smooth transaction. Title companies and attorneys can provide invaluable assistance in this process.

Title companies specialize in researching property records and identifying any outstanding liens or encumbrances on the property. They have access to various databases and resources that allow them to conduct thorough title searches. By hiring a reputable title company, you can gain peace of mind knowing that any existing liens will be uncovered and properly addressed before the sale.

Attorneys, particularly those specializing in real estate law, can also play a significant role in lien research and resolution. They have a deep understanding of the legal intricacies surrounding liens and can provide expert guidance on how to handle different types of liens. Attorneys can negotiate with lien holders, draft necessary legal documents, and ensure that the lien release process is carried out correctly.

It’s important to note that engaging the services of title companies and attorneys comes with associated costs. Title companies typically charge fees for their research and title insurance, which can vary depending on the property value and location. Attorneys’ fees can also vary based on their hourly rates and the complexity of the lien resolution process.

While these costs may seem significant, they are often a worthwhile investment to ensure a smooth and legally compliant sale. Attempting to navigate the lien resolution process without professional assistance can lead to costly mistakes, delays, or even the termination of the sale. By working with experienced professionals, you can mitigate risks and ensure that any existing liens are properly addressed before transferring ownership of the property.

Documenting Lien Resolutions and Obtaining Formal Releases

When selling a house with existing liens, it’s crucial to properly document the resolution of those liens and obtain formal releases. Failure to do so can lead to legal complications and potential ownership disputes down the line.

Depending on the type of lien, the process for resolving it may vary. For instance, if you have a mortgage lien, you’ll need to work with your lender to satisfy the outstanding balance and obtain a release of the lien. Tax liens, on the other hand, typically require payment of the owed taxes, plus any applicable fees or interest, to the relevant government authority.

Regardless of the lien type, it’s essential to maintain thorough documentation of all communications, payments, and agreements related to the lien resolution process. This paper trail will serve as evidence that the lien has been properly addressed and can be presented to the buyer or their representatives if needed.

Once the lien has been satisfied, you should request a formal release document from the lien holder. This document officially acknowledges that the lien has been removed from your property and should be recorded with the appropriate government agency, such as the county recorder’s office.

It’s also advisable to obtain a title report or lien search from a reputable title company to ensure that no other undisclosed liens exist on the property. This extra step can provide added peace of mind and help prevent any surprises during the closing process. If you’re thinking, I need to “Sell My House Fast in Richmond, VA“, RVA Home Buyers with over 25 years of local market expertise selling vacant homes can help.

Call Us Now – (804) 420-8515